Feitelijk Gecontroleerd

Feitelijk Gecontroleerd

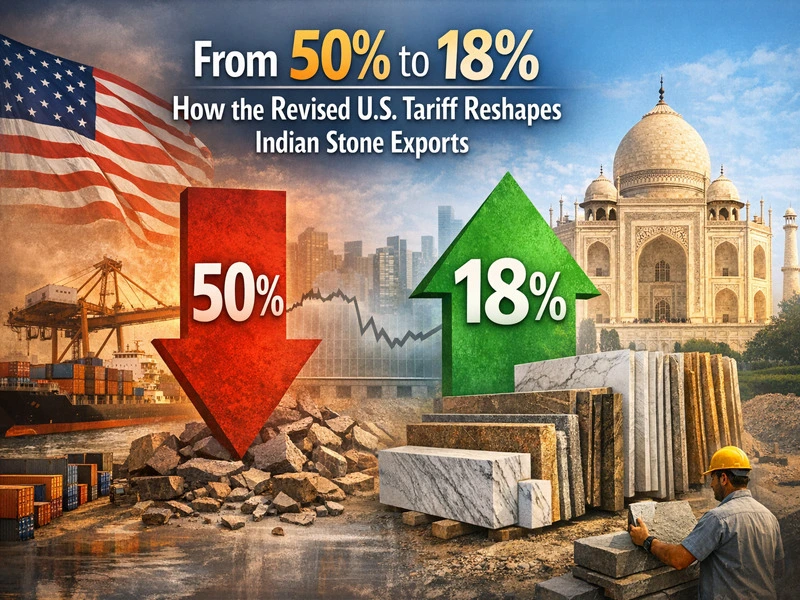

After months of disruption caused by steep trade barriers and following the removal of a 25% additional duty imposed under Russia-related emergency measures, and the recalibration of reciprocal tariffs under Executive Order 14257, Indian-origin goods are now subject to an 18% reciprocal tariff rate. While this reduction offers much-needed relief to exporters and importers alike, it does not simply restore the market to pre-2025 conditions.

The revised tariff changes pricing dynamics, sourcing decisions, and competitive positioning — but it also leaves behind important lessons from the 2025 shock that continue to shape strategy today.

This article explains what has changed, what has not, and how Indian granite, marble, and quartzite exporters should interpret the new 18% duty in practical terms.

A Quick Recap: The 2025 Tariff Shock

Between April and August 2025, the United States sharply increased import duties on Indian natural stone, raising tariffs from the earlier range of 0%–3.7% to as high as 50% under a combination of reciprocal and additional trade measures.

The impact was immediate. Shipments were delayed or canceled, existing contracts came under pressure, and export margins were severely disrupted. In the weeks following the tariff’s implementation, exports to the U.S. declined noticeably as buyers reassessed sourcing decisions and pricing viability.

Faced with the sudden cost shock, Indian exporters were forced to pause shipments, explore alternative markets, and renegotiate terms with long-standing U.S. customers.

Related analysis | Detailed review of the 2025 tariff escalation

What Has Changed With the 18% Tariff?

On 2nd February 2026, the United States announced the removal of the additional 25% duty and a recalibration of the reciprocal tariff from 26% to 18%, materially reducing total effective exposure from the peak levels seen in 2025. The revision applies with immediate effect.

As the decision is recent, detailed notifications and implementation guidelines are still emerging. However, initial discussions and market responses appear reassuring, indicating a shift away from the extreme disruption seen during the 2025 tariff period.

The recent tariff shifts can be summarised as follows:

Evaluating Indian Stone Under the New U.S. Duty?

Speak With Our Export TeamDiscuss volume pricing, container planning, and duty-adjusted landed cost for your upcoming shipment.

| Period | Tariff Regime | Impact |

|---|---|---|

| Pre-April 2025 | Normal MFN tariffs (low/0-5%) | Competitive |

| April 2025 (EO 14257) | India reciprocal tariff set at 26% | Elevated |

| Aug 2025 (Plus EO 14329) | Add’l 25% sanctions duty stacked | Total ~50%+ tariffs |

| Feb 2026 (Framework / EO 14384) | Sanctions duty removed; reciprocal tariff reduced to 18% | Relief, but not a full reset |

This change signals a new reality, with clearer trade patterns expected to emerge as further details and shipment data become available.

What the 18% Tariff Solves — and What It Doesn’t

The reduction in combined tariff exposure — following removal of the 25% additional duty and the adjustment of the reciprocal tariff to 18% — addresses some immediate pressures, but it does not eliminate all structural challenges.What the 18% Tariff Helps Solve

1. Reduces Extreme Cost Shock: The lower duty eases the sharp price increase created by the 50% tariff, allowing trade to resume on a more workable basis.

2. Restores Partial Price Competitiveness: Indian granite, marble, and quartzite regain some competitiveness in the U.S. market compared with the peak tariff period.

3. Enables Order Restart and Negotiation: Projects and contracts paused during the 50% tariff phase can be renegotiated or reactivated under more realistic pricing conditions.

4. Improves Cash Flow Predictability: With lower duty volatility, exporters and importers can plan shipments and pricing with greater certainty.

What the 18% Tariff Does Not Solve

1. Does Not Restore Pre-2025 Conditions: Tariffs remain significantly higher than the earlier 0%–3.7% range, keeping pressure on margins.

2. Does Not Eliminate Market Risk: Dependence on a single export market still exposes exporters to future policy changes.

3. Does Not Guarantee Volume Recovery: While demand may stabilize, shipment volumes may not return to earlier peaks immediately.

4. Does Not Replace the Need for Strategic Change: Value addition, diversification, and operational efficiency remain essential for long-term competitiveness.

How the Revised Tariff Changes Export Strategy

One of the biggest challenges for Indian stone exporters is recovering pricing. During the high-tariff period, intense pressure to sustain operations forced many exporters to reduce prices sharply or liquidate inventory at a loss, as the entire supply chain adjusted to the new cost reality.

Looking for Updated Granite Export Pricing?

Request Latest Price ListReceive current FOB pricing, shipment timelines, and guidance under the revised 18% duty.

As demand gradually returns, restoring prices to earlier levels — or even returning to sustainable profitability — will be difficult. Buyers have adjusted expectations based on discounted pricing during the tariff period, making price correction a slow and sensitive process rather than an immediate recovery.

What This Means for U.S. Importers & Buyers

The United States has implemented import tariffs across a wide range of countries, not only India. With the revised 18% tariff, Indian natural stone becomes competitive again in the U.S. market, especially when compared with other global suppliers facing similar or higher duties.

With the reduced tariff, imports from India are financially workable again for a wider range of residential and commercial projects.

However, buyers adjusted expectations during the high-tariff period, when discounted pricing became common. As exporters continue to recover from earlier losses, price correction is inevitable, but it is likely to be gradual rather than sudden, as the market works back toward sustainable pricing levels.

How Indian Exporters Should Read This Moment

The tariff episode highlighted the risks of over-dependence on a single market. Even with improved access to the U.S., exporters should continue building presence across multiple regions.

The 2025 tariff shift demonstrated how quickly trade conditions can change. Export strategies should treat policy uncertainty as a constant and build flexibility into operations and planning.

Businesses should be structured so that future trade disruptions do not create the same level of stress again. While the recent impact originated in the U.S., similar risks could emerge from any market.

The focus must remain on building sustainable and profitable operations, rather than chasing volume or relying on markets that appear easy to access in the short term. Diversification, value addition, and pricing discipline are essential to reduce vulnerability.

Most importantly, the strategic momentum developed during the recent disruption should not be lost. Preserving these improvements is critical for long-term stability and resilience.

Conclusion

The U.S. tariff reduction from 50% to 18% is an important relief for Indian stone exporters — it narrows the gap created by the 2025 shock and makes many exports financially workable again. At the same time, 18% is not a return to the pre-2025 tariff environment (0%–3.7%) and remains above the preferential or MFN levels some importers see in other markets. Tariff exposure is now a structural feature of global trade policy, not an exception: the U.S. has adjusted duties across multiple sourcing countries, while other importing countries apply a range of duties depending on HS/CN/HTS lines.

For exporters, the practical lesson is unchanged: treat the reduced duty as stabilisation, not a reset. Maintain diversification, prioritise value-added products and pricing discipline, and preserve the operational improvements gained during the disruption — those steps will protect margins and resilience whether tariffs rise again or settle at new baselines.